March 2025 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full March 2025 dataset — every named company, round, investor, and segment.

What March told us

March 2025 is the month the modern cybersecurity M&A era was unambiguously priced. Google announced its $32 billion acquisition of Wiz — the largest cybersecurity transaction ever, full stop, and roughly 3x the next-largest precedent in this dataset. A single deal of that size reframes everything else in the month and arguably everything else in the year: $1.02B in disclosed private funding looks substantial in most contexts, but it's two-and-a-half percent of what Wiz alone was worth at exit. Capital is not the constraint in this market. Category leadership is.

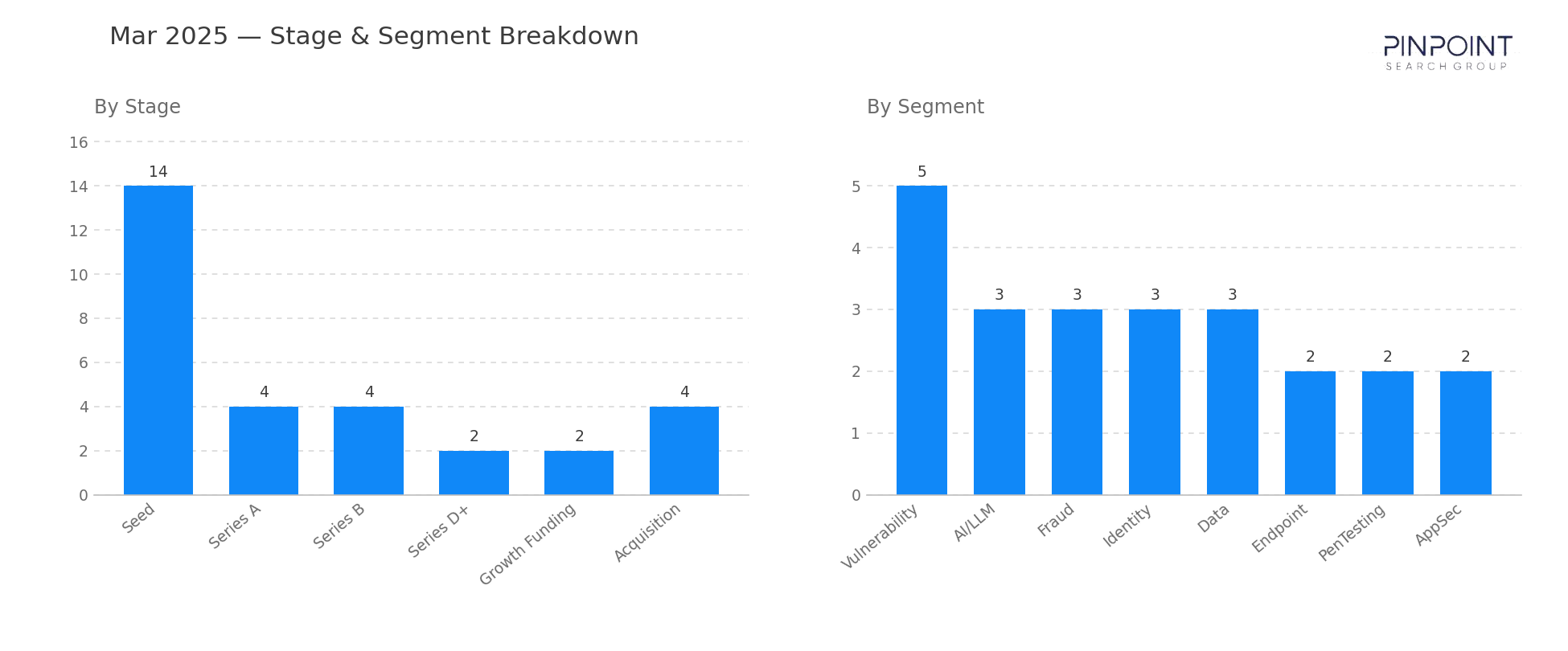

Setting the megadeal aside, the funding picture itself was strong. $1.02B in disclosed capital across 29 rounds matches the strongest months of 2024, and it came with a tilt back toward the growth end of the curve: Island's $250M Series D for the enterprise browser, Aura's $140M Series D in consumer identity, Cybereason's $120M growth round in endpoint, and Pentera's $60M Series D+ in pentesting. The Seed-and-Series-A pace held at 62% of rounds, but for the first time since mid-2024 there were enough late-stage checks above $100M to suggest growth-stage investors are unfreezing on the segments they believe have buyer optionality.

Vulnerability led the segment mix with 5 transactions — anchored by SpecterOps' $75M Series B and rounded out by four smaller deals (VulnCheck's $12M Series A among them) — followed by AI/LLM, Fraud, Identity, and Data tied at 3 each. The other three M&A transactions all matter, even sitting next to a $32B headline: Jamf paid $215M for Identity Automation, Armis paid $120M for Otorio in OT/ICS, and Wiz itself, days before its own announcement, was an active buyer too. The signal: the top tier of cyber vendors continues to roll up adjacent capabilities, and the platforms that emerge from this cycle will be three to five very large hyperscaler-adjacent suites, not the dozen-plus pure-plays that defined the 2018–2022 era.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 14 |

| Series A | 4 |

| Series B | 4 |

| Series D+ | 3 |

| Growth Funding | 4 |

| Acquisition | 4 |

| Top segments | Transactions |

|---|---|

| Vulnerability | 5 |

| AI/LLM | 3 |

| Fraud | 3 |

| Identity | 3 |

| Data | 3 |

| Endpoint | 2 |

Two deals worth your attention

Google's $32B acquisition of Wiz. Google Cloud's all-cash acquisition of cloud security platform Wiz is the largest cybersecurity transaction in history and Google's largest acquisition of any kind. Wiz had been publicly resisting acquisition since rejecting Google's first $23B offer in mid-2024; the renegotiated terms — and the regulatory landscape post-2024 election — appear to have closed the gap. The strategic logic is straightforward: hyperscalers selling cloud capacity need to sell the security layer alongside it, and the cleanest way to acquire that capability at scale is to buy the leading cloud-native security platform outright.

Island — $250M Series D+ led by Coatue. Island's enterprise browser raised $250M at growth-stage valuations led by Coatue. The round is notable not only for its size but for what it implies about the browser-as-security-perimeter thesis: the enterprise browser segment, which barely existed in 2022, has now produced one of the largest Series D rounds in cybersecurity this cycle.

Companies we've covered before

Wiz first appeared in December 2020 with a $100M Series A in Cloud security — already one of the largest Series A rounds in the workbook. Six appearances and 51 months later, it exits to Google for $32B, the largest cybersecurity acquisition ever recorded in this series.

Island first appeared in March 2022 with a $115M Series B in Browser security. Three years and two rounds later, it returns with a $250M Series D in the same segment — the cleanest growth-stage arc in the enterprise browser category.

The other 31 transactions are in the data feed — including the 4 acquisitions whose values never hit the press. Get March's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.