August 2025 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full August 2025 dataset — every named company, round, investor, and segment.

What August told us

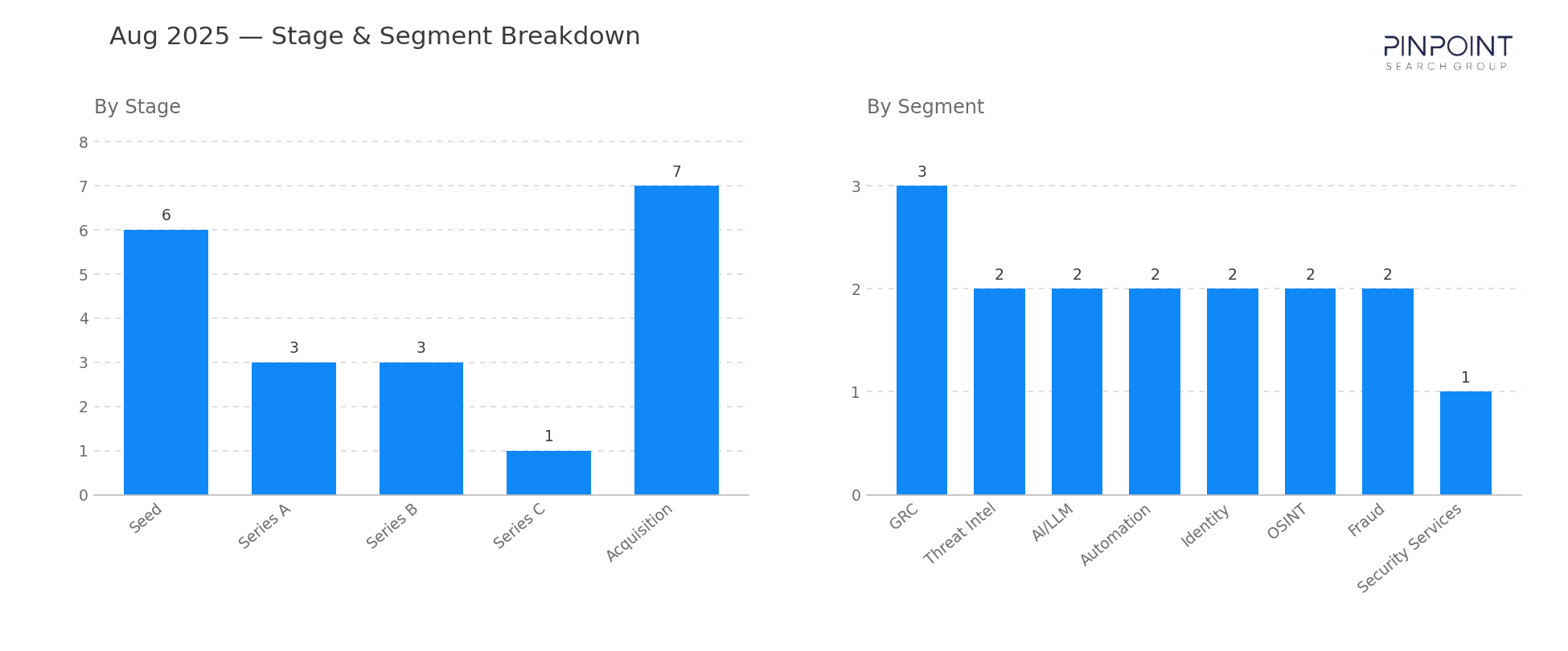

August 2025 was the quietest cyber funding month of the year. Total transactions fell to 22 — less than half the July pace — and disclosed funding capital dropped to $440M, down 51% from August 2024's $904M. The drop is partly seasonal (August is consistently among the lowest-volume months in this series) and partly composition: only one Series D+ round cleared and only one growth round. The market took its annual breath.

Where capital did move, it concentrated in three large Series B and C rounds: Ontic's $230M Series C in OSINT/protective intelligence (the largest funding event of the month and the highest single round we have tracked in the OSINT segment), IVIX at $60M in OSINT, and Seemplicity at $50M in automation. The seed-and-Series-A share was 60% of rounds — within the normal band — but the funding-round count of 15 is the lowest of the year so far and worth flagging.

Counterintuitively, M&A held up better than funding. Seven acquisitions cleared, four of them with disclosed values totaling $1.34B. Accenture paid $649M for CyberCX (Australian security services). Diginex paid $305M for Findings in GRC. CrowdStrike paid $290M for Onum in threat intelligence pipelines, and Okta paid $100M for Axiom in non-human identity. The combined signal: even in a quiet funding month, the consolidation engine kept running, and the platform vendors continued to absorb adjacencies.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 6 |

| Series A | 3 |

| Series B | 3 |

| Series C | 1 |

| Series D+ | 1 |

| Growth Funding | 1 |

| Acquisition | 7 |

| Top segments | Transactions |

|---|---|

| GRC | 3 |

| Threat Intel | 2 |

| AI/LLM | 2 |

| Automation | 2 |

| Identity | 2 |

| OSINT | 2 |

Two deals worth your attention

Ontic — $230M Series C led by KKR. Ontic raised $230M led by KKR for its protective intelligence platform — the largest single funding event of August and the highest-priced round we have tracked in the OSINT segment. The round signals that physical-security-meets-cyber-threat-intelligence is being repriced as enterprise software, with KKR's involvement implying a clear path to either platform consolidation or public market access in 2026–2027.

Accenture's $649M acquisition of CyberCX. Accenture acquired CyberCX, the largest independent cybersecurity services firm in Australia and New Zealand, for $649M. The deal consolidates the APAC cyber-services market under a global integrator and reflects the broader 2024–2025 pattern of professional-services consolidation around regional security specialists — particularly in geographies where local compliance frameworks (Australia's SOCI, NZ's Privacy Act updates) drive sustained demand.

Companies we've covered before

Axiom first appeared in December 2022 with a $7M Seed in Identity. Two and a half years later, it exits to Okta for $100M — a textbook non-human identity consolidation arc.

Prompt Security first appeared in January 2024 with a $5M Seed in AI/LLM. Eighteen months later, the company is acquired (undisclosed value) — one of the fastest seed-to-acquisition arcs in the workbook and a marker of how aggressively the AI security category is consolidating.

The other 20 transactions are in the data feed — including the 7 acquisitions whose values never hit the press. Get August's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.