June 2025 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full June 2025 dataset — every named company, round, investor, and segment.

What June told us

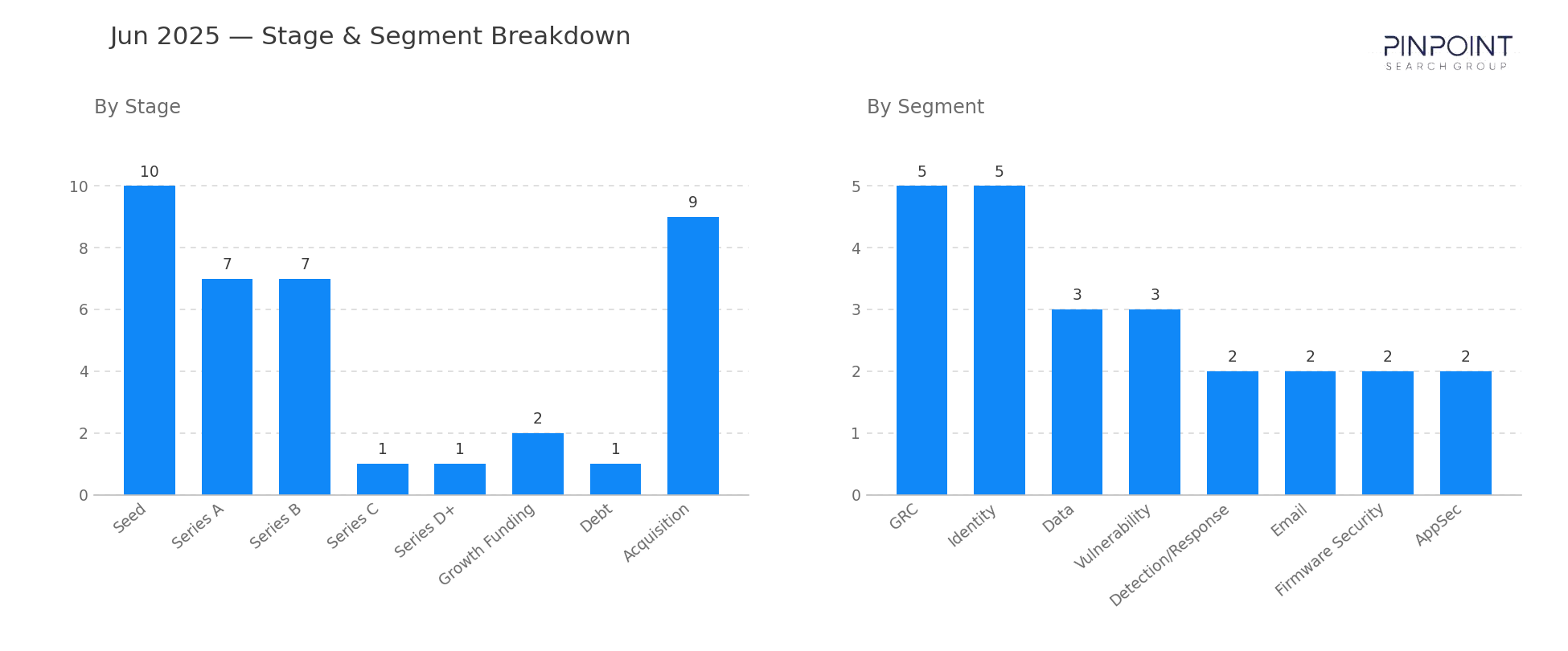

June 2025 produced $994M in disclosed funding across 29 rounds — modestly above June 2024 — alongside a notable jump in M&A volume to 9 acquisitions, the highest count of the year so far. Funding was again top-heavy: Cato Networks' $359M growth round in SASE accounted for 36% of the month's disclosed capital, and the next four rounds (Clearspeed at $60M, Zama at $57M, Guardz at $56M, Zero Networks at $55M) clustered in the same growth-but-not-huge band.

The segment mix was led by GRC (5) and Identity (5), with Data and Vulnerability tied at 3 each and Detection/Response and Email at 2. The notable composition feature: only one Series D+ round cleared in the entire month, against two growth rounds. That is the inverse of February-March's pattern and reads as the late-stage market pausing after April's burst, while growth-equity continues to absorb the companies that don't want to mark up to traditional growth-VC pricing.

Nine acquisitions cleared, and only Cellebrite's $190M acquisition of Corellium came with a disclosed price. The Cellebrite–Corellium deal — digital forensics buying ARM virtualization for mobile research — is a niche but strategically clean combination that signals the digital forensics category continues to consolidate around the major players. The other eight deals were undisclosed, which is now the standard pattern: 80%+ of monthly M&A clears without a public price tag.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 10 |

| Series A | 7 |

| Series B | 7 |

| Series C | 1 |

| Series D+ | 1 |

| Growth Funding | 2 |

| Debt | 1 |

| Acquisition | 9 |

| Top segments | Transactions |

|---|---|

| GRC | 5 |

| Identity | 5 |

| Data | 3 |

| Vulnerability | 3 |

| Detection/Response | 2 |

| 2 |

Two deals worth your attention

Cato Networks — $359M growth round in SASE. Cato Networks' SASE platform raised $359M, taking the company past $700M in cumulative known capital across four appearances in this series. The round, with growth-equity participants, reflects the continued consolidation of the SASE category around four to five large platforms, with Cato positioned as the leading independent.

Cellebrite's $190M acquisition of Corellium. Cellebrite acquired Corellium, the ARM virtualization platform widely used in mobile and IoT security research, for $190M. The combination gives Cellebrite — already the dominant digital forensics vendor in law enforcement — a foothold in pre-incident mobile research tooling and signals that digital forensics is broadening its product surface from incident response into proactive research.

Companies we've covered before

Cato Networks first appeared in November 2020 with a $130M Series D+ round in SASE. Across four appearances since, the company has accumulated roughly $700M in disclosed capital and is now the most heavily capitalized independent SASE vendor in the workbook.

Zama first appeared in March 2024 with a $73M Series A in Data security. Fifteen months later, it returns with a $57M Series B in the same segment — one of the steadier confidential-computing arcs we've tracked.

The other 36 transactions are in the data feed — including the 9 acquisitions whose values never hit the press. Get June's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.