May 2024 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full May 2024 dataset — every named company, round, investor, and segment.

What May told us

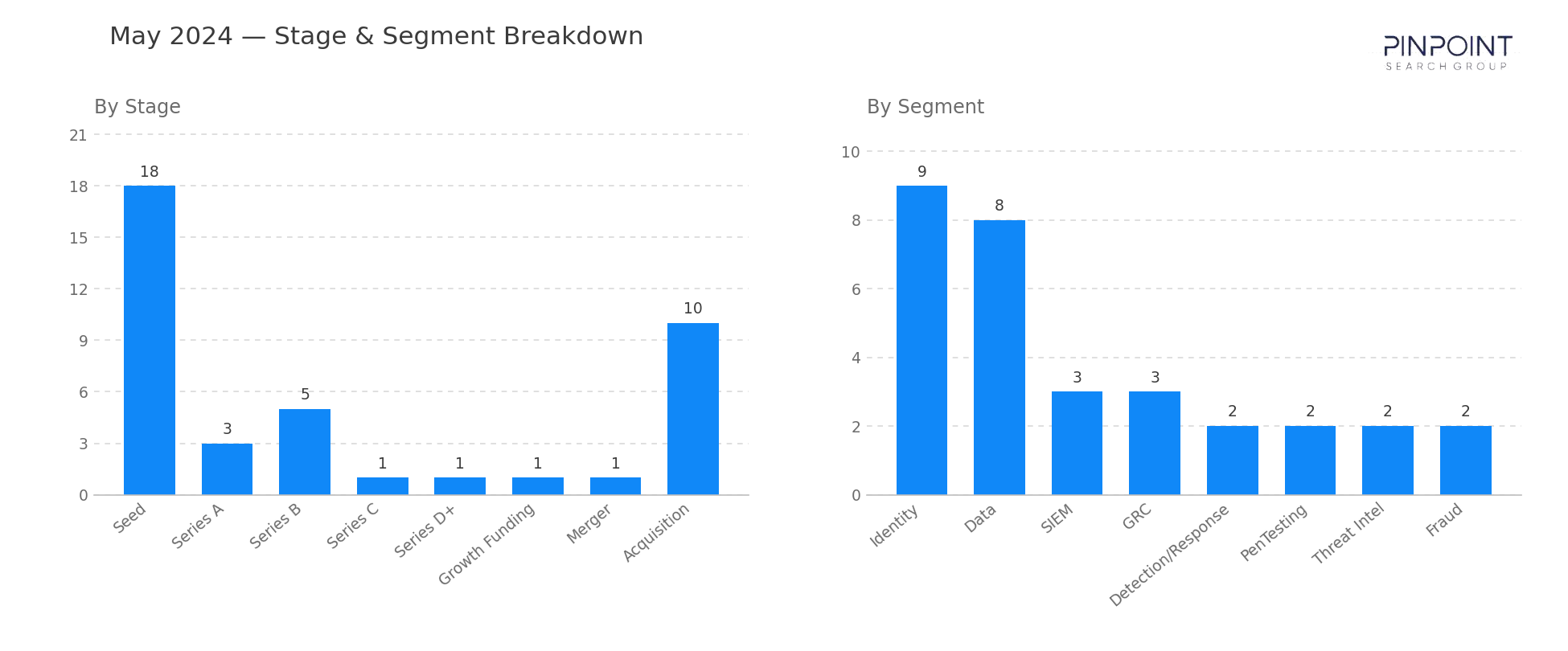

May 2024 stacked an unusual number of large transactions into a single month. Disclosed funding hit $1.48B across 34 rounds, anchored by Wiz's $1B Series E at a $12B valuation — one of only three nine-figure-plus single-round funding events the workbook has tracked, alongside Lacework's $1.3B in 2021 and Securonix's $1B growth round in 2022. Alongside it, three M&A deals over $450M cleared in the same window: Hg's $3B take-private of AuditBoard, CyberArk's $1.54B acquisition of Venafi, and Akamai's $450M acquisition of Noname Security. The combination of late-stage venture and large-cap M&A made May 2024 the most active single month of the year so far.

Wiz's $1B round deserves a separate read. The company's growth path through the workbook — $100M Series A in 2020, $130M and $120M Series B rounds in 2021, $250M Series C in late 2021, $300M Series E in 2023, $1B Series E in 2024 — is the most consistent funding story in cyber, and the May round positions Wiz as the platform vendor able to absorb meaningful M&A. The Gem Security deal in March was the opening strategic signal; the May $1B confirms Wiz can sustain that buyer posture at scale.

Identity took 9 of May's 34 transactions, the largest single-segment count for the month. CyberArk's $1.54B acquisition of Venafi consolidated machine-identity at the largest scale in the segment's history, and the funded rounds in identity skewed toward non-human use cases — Lumos at Series B in identity governance, Oasis Security at Series A in non-human identity, StrongDM at Series C in privileged access. The pattern matches the broader 2024 arc inside identity: capital flowed where humans aren't.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 18 |

| Series A | 3 |

| Series B | 5 |

| Series C | 1 |

| Series D+ | 1 |

| Growth Funding | 1 |

| Merger | 1 |

| Acquisition | 10 |

| Top segments | Transactions |

|---|---|

| Identity | 9 |

| Data | 8 |

| SIEM | 3 |

| GRC | 3 |

| Detection/Response | 2 |

| PenTesting | 2 |

Two deals worth your attention

Wiz — $1B Series E led by Andreessen Horowitz, Lightspeed, and Thrive Capital. Wiz raised $1B at a $12B valuation — one of only three single-round cyber funding events the workbook has tracked at $1B or above (Lacework's $1.3B in 2021 and Securonix's $1B in 2022 are the others). The round positions Wiz as the strategic acquirer to beat in cloud security, with capital reserves capable of absorbing meaningful tuck-in M&A; the Gem Security deal in March was the dry run, and the May $1B sustains that buyer posture into the rest of the year.

Hg's $3B take-private of AuditBoard. Hg agreed to acquire AuditBoard at $3B, the second-largest cyber M&A event of 2024 after the Darktrace deal in April. The GRC segment had been one of the more dormant venture categories through 2023; AuditBoard's exit reset the comp set and contributed to a measurable uptick in GRC funding rounds across the back half of 2024.

Companies we've covered before

Wiz first appeared in December 2020 with a $100M Series A in Cloud, returning across five subsequent rounds in 2021–2023 and culminating in the May 2024 $1B Series E. Across six tracked rounds spanning four years, Wiz has stayed in the Cloud segment without reclassification — the cleanest large-scale single-segment arc in the workbook.

Venafi first appeared in December 2020 with a P/E funding event in Endpoint (its then-classification under machine identity). The May 2024 $1.54B exit to CyberArk closes one of the longer full-cycle arcs in the workbook — from private-equity recapitalization to strategic acquisition by the largest pure-play in identity.

The other 42 transactions are in the data feed — including the 10 acquisitions whose values never hit the press. Get May's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.