May 2025 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full May 2025 dataset — every named company, round, investor, and segment.

What May told us

May 2025 produced $1.13B in disclosed funding across 25 rounds — solid but down 24% year-over-year — and a notable shift in where the capital landed. Two transactions, Cyera's $500M growth round in data security and Persona's $200M Series D+ in identity, accounted for 62% of the monthly total. That concentration is the highest of any month in the prior twelve, and it reflects the broader 2025 pattern: capital is becoming bimodal, with seed funding plentiful and growth funding scarce but enormous when it lands.

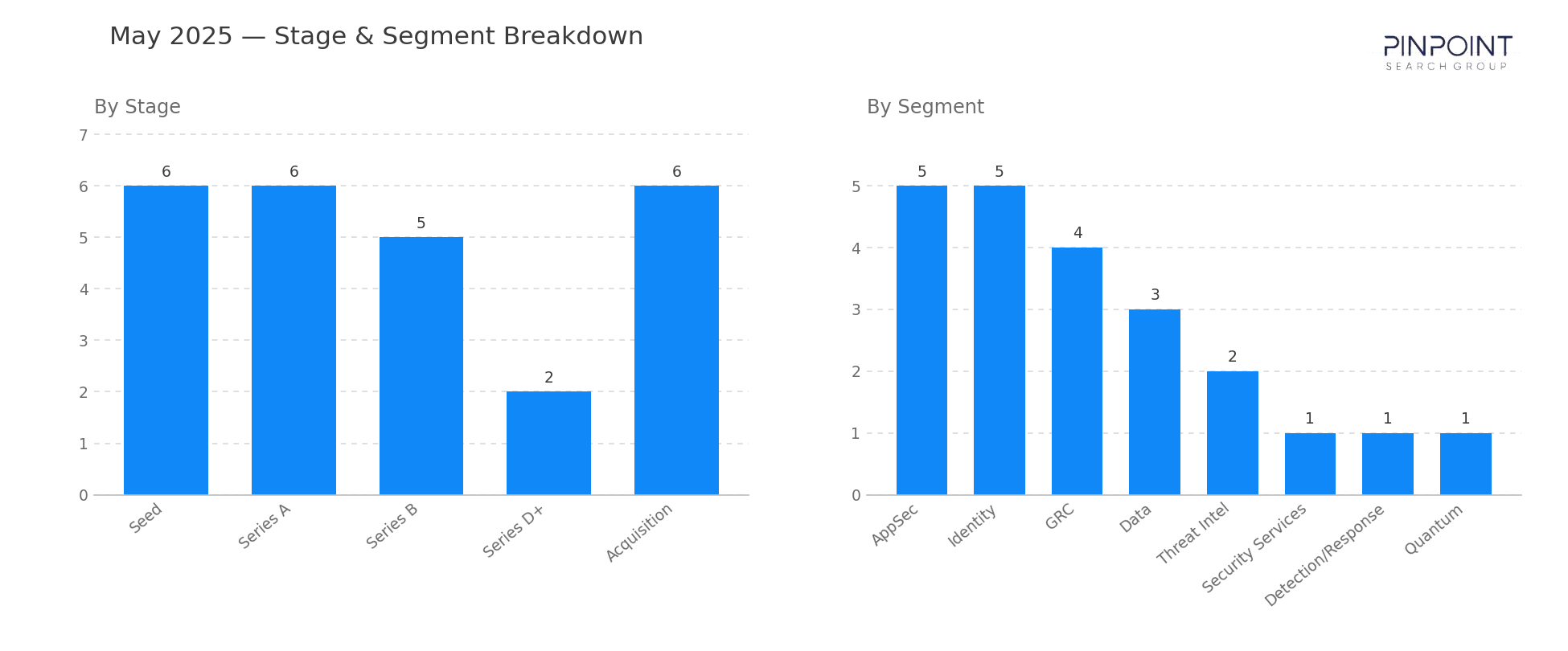

The seed-and-Series-A share dropped to 48% of rounds, the lowest in three months. That is not a deterioration; it is a composition effect. Late-stage rounds were heavier this month and the early-stage pace simply did not match April's surge. AppSec (5) and Identity (5) tied at the top of the segment mix, with GRC (4) and Data (3) close behind. Data's headline number was carried entirely by Cyera's $500M round; the other two Data deals were sub-$30M each.

M&A is where the structural story lives. Proofpoint's $1.8B acquisition of Hornetsecurity is the largest disclosed M&A value we have tracked in the email and security-services space since 2020, and folds a European MSP-focused email security and backup platform into Proofpoint's portfolio. Check Point's $100M acquisition of Veriti adds preemptive security posture; Bitdefender bought Mesh Security in the same month. The pattern across all three: incumbent platforms continuing to fill out adjacencies, not the disruptor-on-disruptor M&A that characterized 2021–2022.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 6 |

| Series A | 6 |

| Series B | 5 |

| Series D+ | 2 |

| Growth Funding | 6 |

| Acquisition | 6 |

| Top segments | Transactions |

|---|---|

| AppSec | 5 |

| Identity | 5 |

| GRC | 4 |

| Data | 3 |

| Threat Intel | 2 |

| Security Services | 1 |

Two deals worth your attention

Cyera — $500M growth round led by Georgian. Cyera's data security platform raised $500M led by Georgian. This is Cyera's fifth appearance in this series since 2022 and its largest single round to date. Across five tracked rounds inside Data security, Cyera is now one of the most heavily capitalized private cyber vendors of the cycle and a probable platform acquisition target.

Proofpoint's $1.8B acquisition of Hornetsecurity. Proofpoint, owned by Thoma Bravo since 2021, acquired German-headquartered email security and Microsoft 365 backup vendor Hornetsecurity for a reported $1.8B. The deal expands Proofpoint's footprint in the European mid-market and signals the consolidation of email security into broader 'security services for Microsoft 365' platforms.

Companies we've covered before

Cyera first appeared in March 2022 with a $60M growth round in Data security. Five rounds and 39 months later, it raises a $500M growth round in the same segment — one of the most capitalized data security companies in private cyber.

Veriti first appeared in November 2022 with an $18M Seed in Ratings classification. Two and a half years later it exits to Check Point for $100M — a tidy seed-to-acquisition arc inside the posture management space.

The other 29 transactions are in the data feed — including the 6 acquisitions whose values never hit the press. Get May's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.