2023 Cyber Security Vendor Funding Report

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

2023 Cyber Security Vendor Transaction Highlights

Get the full 2023 dataset — every named company, round, investor, segment, and acquisition.

Crunching the Numbers

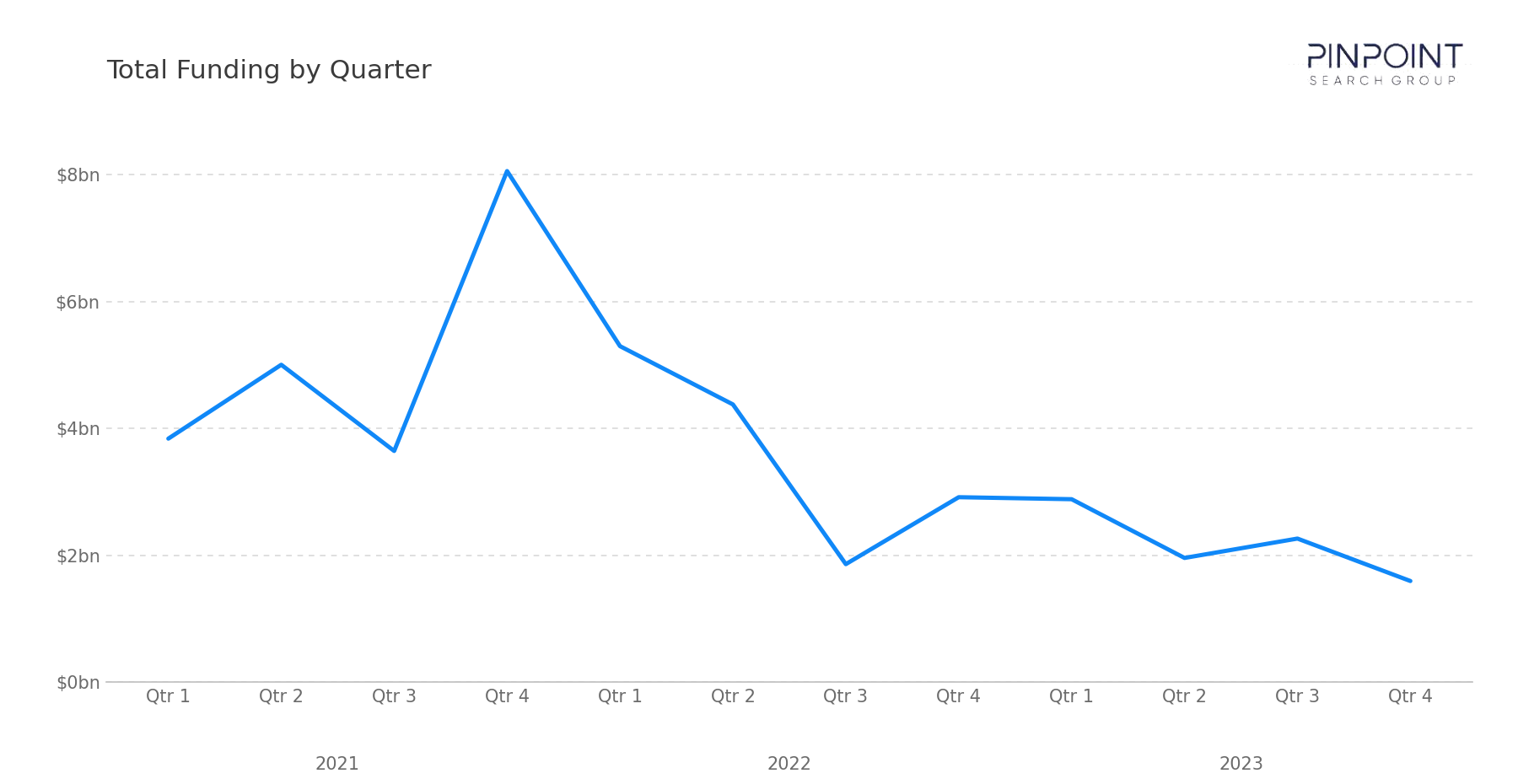

- The $8.70B raised in FY 2023 represents a 40% decrease in funding raised compared to 2022 ($14.45B).

- Funding volume increased by 13% with 347 funding rounds tracked in FY 2023 compared to 307 in 2022.

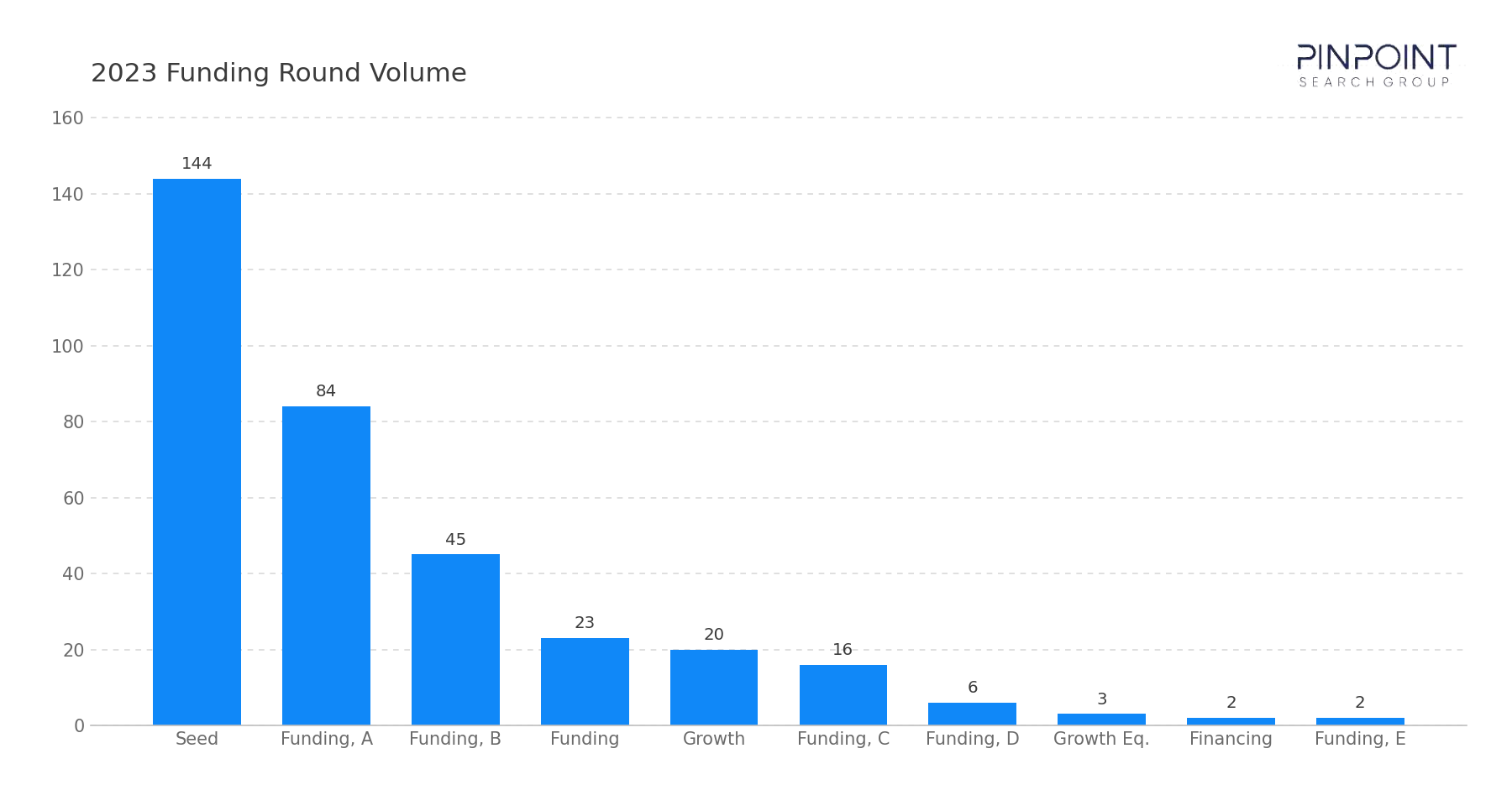

- Early-stage funding (Seed, Series A) represented 66% of total funding volume.

- 20 funding rounds above $100M accounted for 41% of all capital raised while representing just 6% of funding volume.

Join our mailing list to receive quarterly report analysis

Highlights and Analysis

In 2023 our team tracked $8.7 billion in disclosed cybersecurity vendor funding across 347 rounds, a 40% decline from 2022 — the sharpest annual pullback the workbook has recorded. The contraction concentrated at the top: only 20 rounds of $100 million or more, accounting for 41% of dollars, against 42 such rounds the year before. Early-stage activity moved the other way — Seed and Series A together made up 66% of all rounds.

The M&A column was dominated by a single transaction. Cisco's $28 billion acquisition of Splunk was the largest cyber acquisition the workbook has tracked, more than seven times the next-largest deal of the year. Splunk's SIEM and machine-data analytics sit squarely in the security stack, and the deal accounted for roughly two-thirds of the year's $42.22 billion in disclosed M&A on its own.

Beneath the Splunk deal, private-equity consolidation continued and managed-services roll-ups accelerated. Thales acquired Imperva for $3.7 billion, TPG carved out Forcepoint's government business for $2.5 billion, and three more public vendors — Sumo Logic, Magnet Forensics, and Absolute Software — went private to sponsors.

Funding Overview

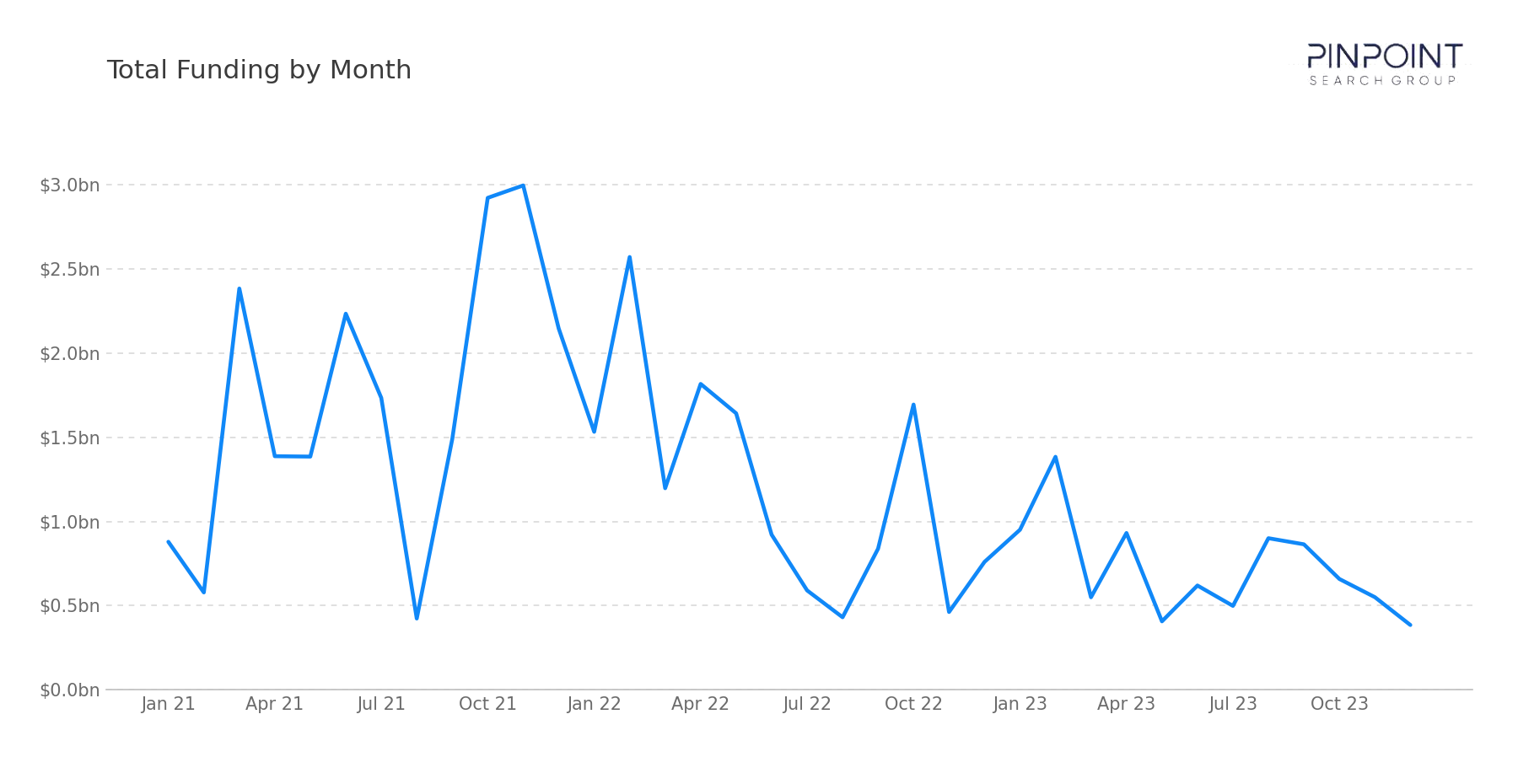

The $8.7 billion is the funding low of the recovery period. Capital did not stop — at 347 rounds, 2023 had the highest round count in the workbook through that point — but it shifted decisively toward the early stage and away from the large late-stage rounds that defined 2021 and early 2022. Quarterly funding ran in a narrow band, from $1.59 billion in Q4 to $2.88 billion in Q1.

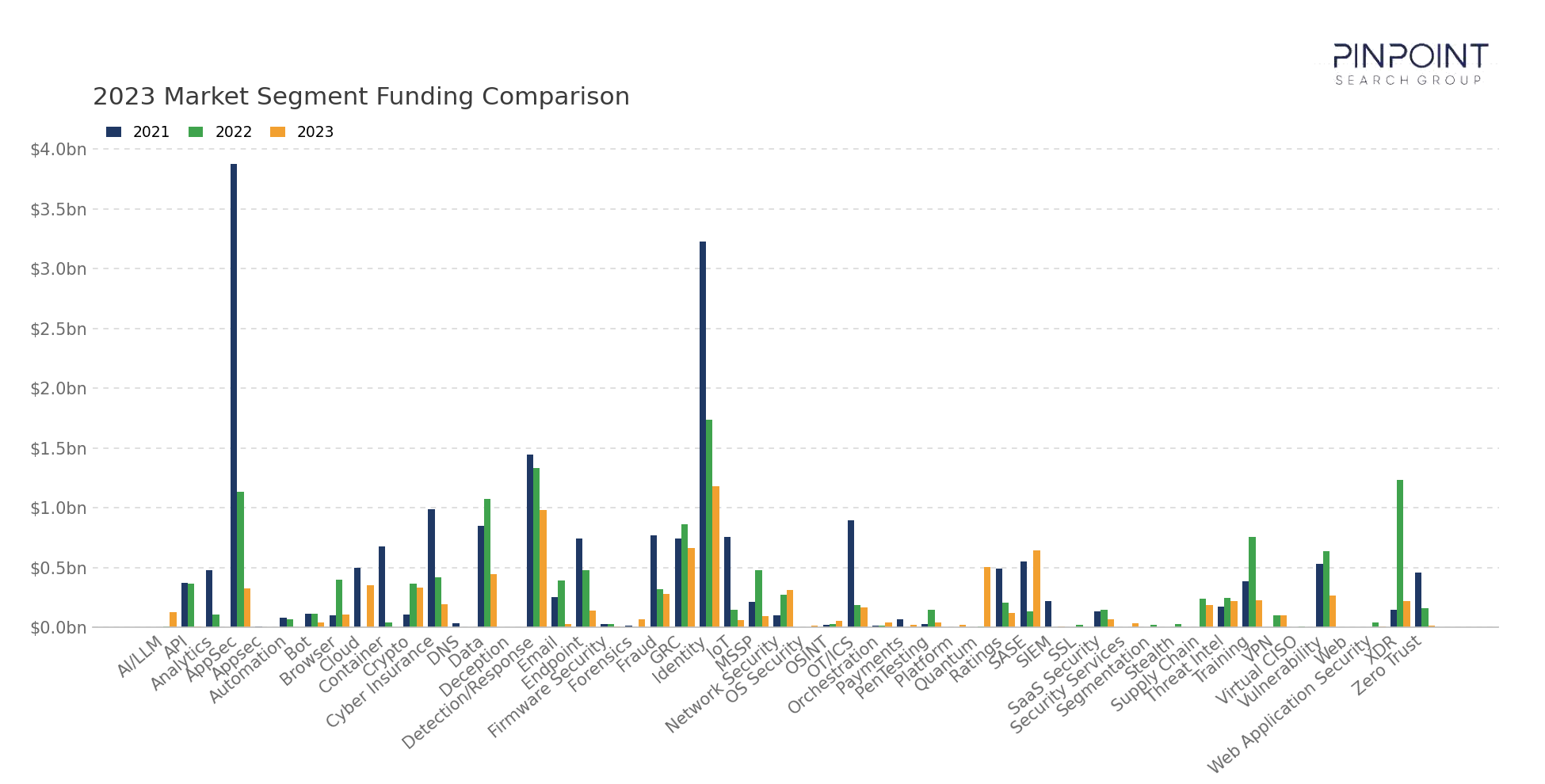

With fewer large rounds, capital clustered in a handful of categories:

- Emerging deep-tech drew the largest rounds — SandboxAQ's $500 million Series B (quantum security) was the year's biggest, ahead of Netskope's $401 million growth round (SASE).

- Cloud security held conviction — Wiz raised $300 million (Series D), continuing to attract late-stage capital against the broader pullback.

- Identity led on round count — $1.18 billion across 46 rounds, the most active segment by number of deals even as single-round sizes shrank.

- Early-stage formation expanded — 228 Seed and Series A rounds, the broad base that absorbed the year's volume as late-stage capital thinned.

The shift to early stage is the defining feature of 2023's funding. The market kept forming companies; it stopped writing the largest checks.

Market & Macro Signals

Several dynamics defined a lean funding year.

Strategic platform consolidation reached new scale. Cisco's $28 billion acquisition of Splunk folded SIEM and observability into a networking-and-security platform — the largest cyber acquisition the workbook has tracked.

PE take-privates continued. Sumo Logic (Francisco Partners, $1.7 billion), Magnet Forensics (Thoma Bravo, $1.34 billion), and Absolute Software (Crosspoint, $870 million) took three more public vendors private.

Managed services consolidated rapidly. MSSP and MSP roll-ups ran at a high pace through the year — many targets small and regional, but the cumulative activity reshaped the category.

Funding moved early. With late-stage capital scarce, Seed and Series A carried the year's volume; large growth rounds were the exception rather than the norm.

M&A Activity & Strategic Moves

Disclosed M&A reached $42.22 billion across 27 priced transactions (of 90 total), but the distribution was extraordinarily top-heavy. Cisco's $28 billion acquisition of Splunk — the largest cyber acquisition the workbook has tracked — accounted for roughly two-thirds of the disclosed total on its own.

Setting Splunk aside, the priced deals group as follows:

- Strategic buyers acquired platforms. Thales/Imperva ($3.7 billion) brought a data-and-application security platform under a defense-and-technology strategic.

- PE carve-outs and take-privates continued. TPG carved out Forcepoint's government business ($2.5 billion); Sumo Logic, Magnet Forensics, and Absolute Software went private to sponsors.

- Strategic tuck-ins filled platform gaps. Palo Alto Networks acquired Talon ($615 million), folding enterprise browser security into its platform.

- Managed-services roll-ups multiplied. A stream of MSSP and MSP acquisitions — mostly undisclosed — consolidated regional providers through the year.

Two patterns coexisted: a single category-defining transaction at the very top (Cisco/Splunk) and a long tail of platform consolidation and managed-services roll-ups beneath it. Disclosed M&A dollars were the second-heaviest the workbook has tracked, but almost entirely on the strength of one deal.

No cybersecurity vendor the workbook tracked completed a conventional IPO in 2023. The year's sole public-market listing came via SPAC merger: HUB Cyber Security, an Israeli data-security vendor, went public on Nasdaq (HUBC) through a blank-check combination in March.

Looking Ahead

2023 was the funding trough and the year strategic consolidation reached its largest scale.

Three themes carry into 2024:

- Whether late-stage funding recovers — the early-stage base is broad, but the largest rounds nearly disappeared in 2023.

- Whether strategic platforms keep consolidating — Cisco/Splunk set a scale that reframes what a platform acquisition can be.

- Whether managed-services roll-ups continue — the pace through 2023 points to an enduring structural shift, not a one-year run.

2023 closed with funding at its leanest and consolidation at its largest single scale. The question for 2024 is whether capital returns to the late stage, or whether the early-stage-heavy, consolidation-driven shape of the market persists.

The full 2023 dataset — every named company, round, investor, segment, and acquisition — is in the data feed. Get the full 2023 dataset →

Methodology

Every transaction in this report was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available. Figures are workbook-derived and reflect ongoing corrections, so they may differ slightly from the originally published 2023 report.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.