2024 Cyber Security Vendor Funding Report

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

2024 Cyber Security Vendor Transaction Highlights

Get the full 2024 dataset — every named company, round, investor, segment, and acquisition.

Crunching the Numbers

- The $9.52B raised in FY 2024 represents a 9% increase in funding raised compared to 2023 ($8.70B).

- Funding volume decreased by 12% with 307 funding rounds tracked in FY 2024 compared to 347 in 2023.

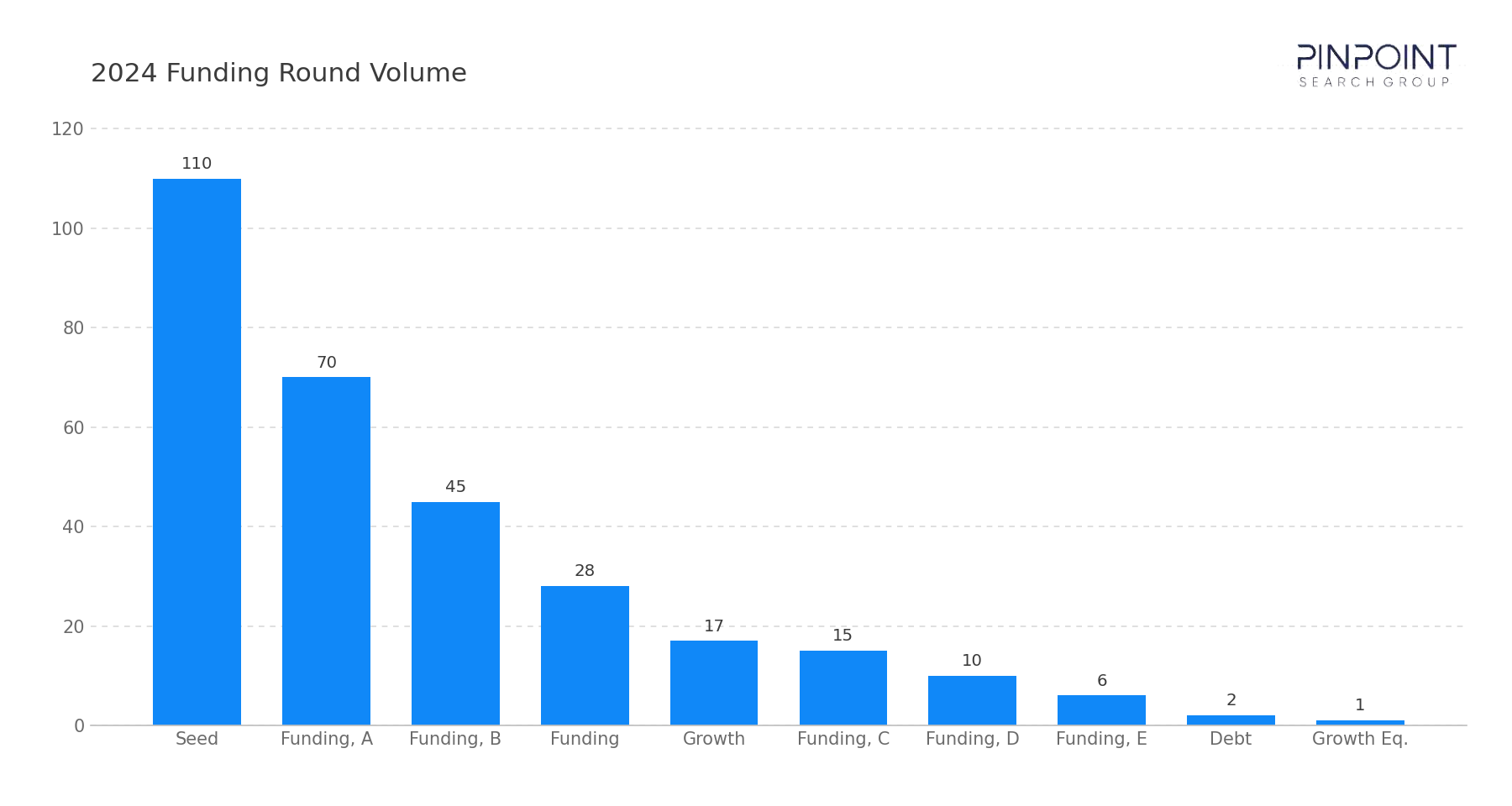

- Early-stage funding (Seed, Series A) represented 59% of total funding volume.

- 24 funding rounds above $100M accounted for 50% of all capital raised while representing just 8% of funding volume.

Join our mailing list to receive quarterly report analysis

Highlights and Analysis

In 2024 our team tracked $9.52 billion in disclosed cybersecurity vendor funding across 307 rounds, a 9% recovery from 2023's trough. The rebound was modest and concentrated: 24 rounds of $100 million or more accounted for half of all dollars, and Wiz's $1 billion Series E — the year's largest round — signaled the return of conviction-led late-stage capital. Seed and Series A held 59% of round volume.

The more telling shift was in who was buying. Rather than a single dominant buyer type, 2024's M&A broadened across cohorts: private-equity take-privates, PE platform roll-ups, a non-cyber strategic deepening its position, and pure-cyber strategics all wrote large checks. Disclosed M&A totaled $17.21 billion across 22 priced deals.

Thoma Bravo's $5.3 billion take-private of Darktrace was the year's largest deal, but the cohort partition tells the story: PE-aligned transactions led (Darktrace plus Hg's $3 billion acquisition of AuditBoard), while Mastercard's $2.65 billion acquisition of Recorded Future extended a non-cyber strategic deeper into threat intelligence and CyberArk's $1.54 billion purchase of Venafi represented pure-cyber strategic consolidation.

Funding Overview

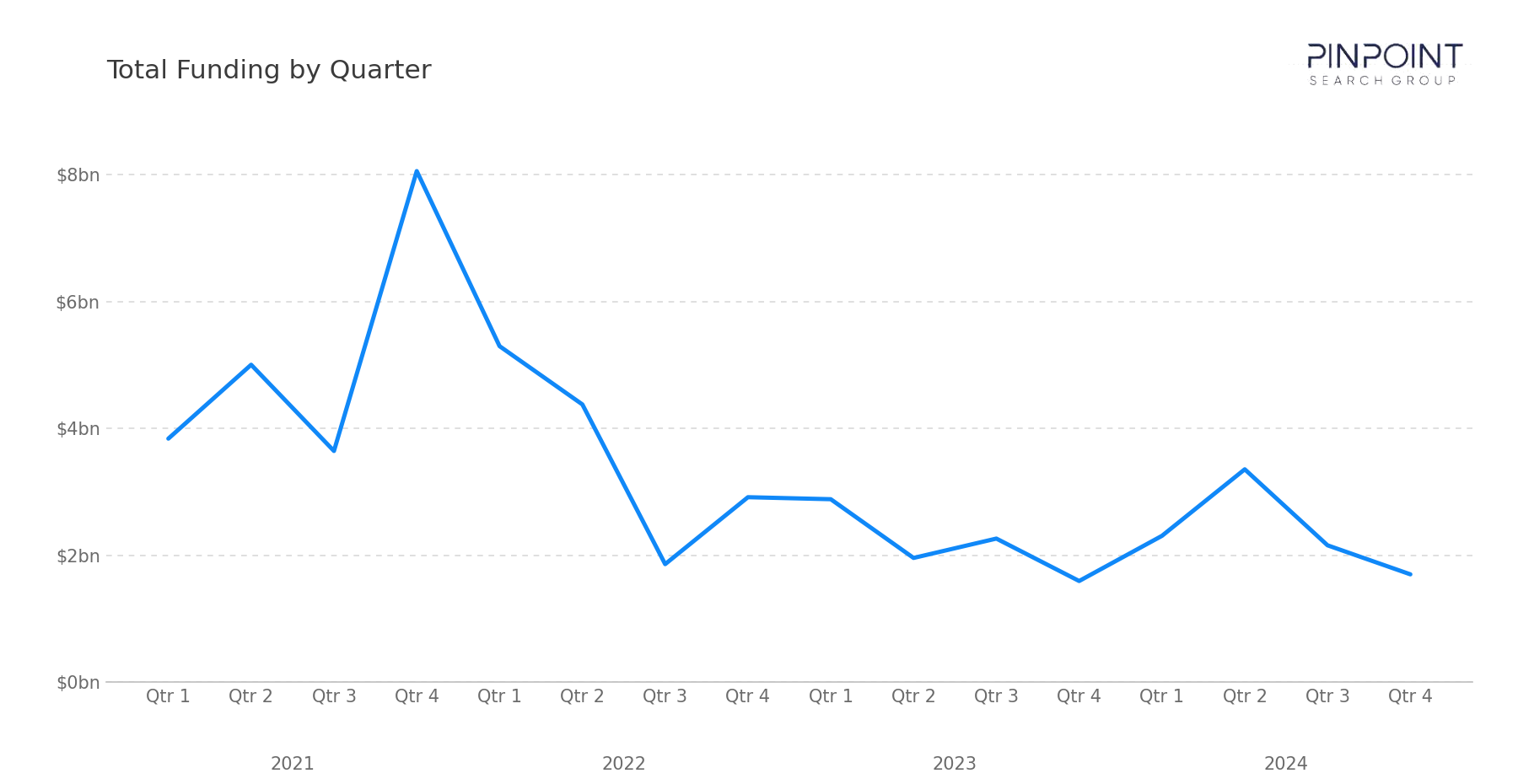

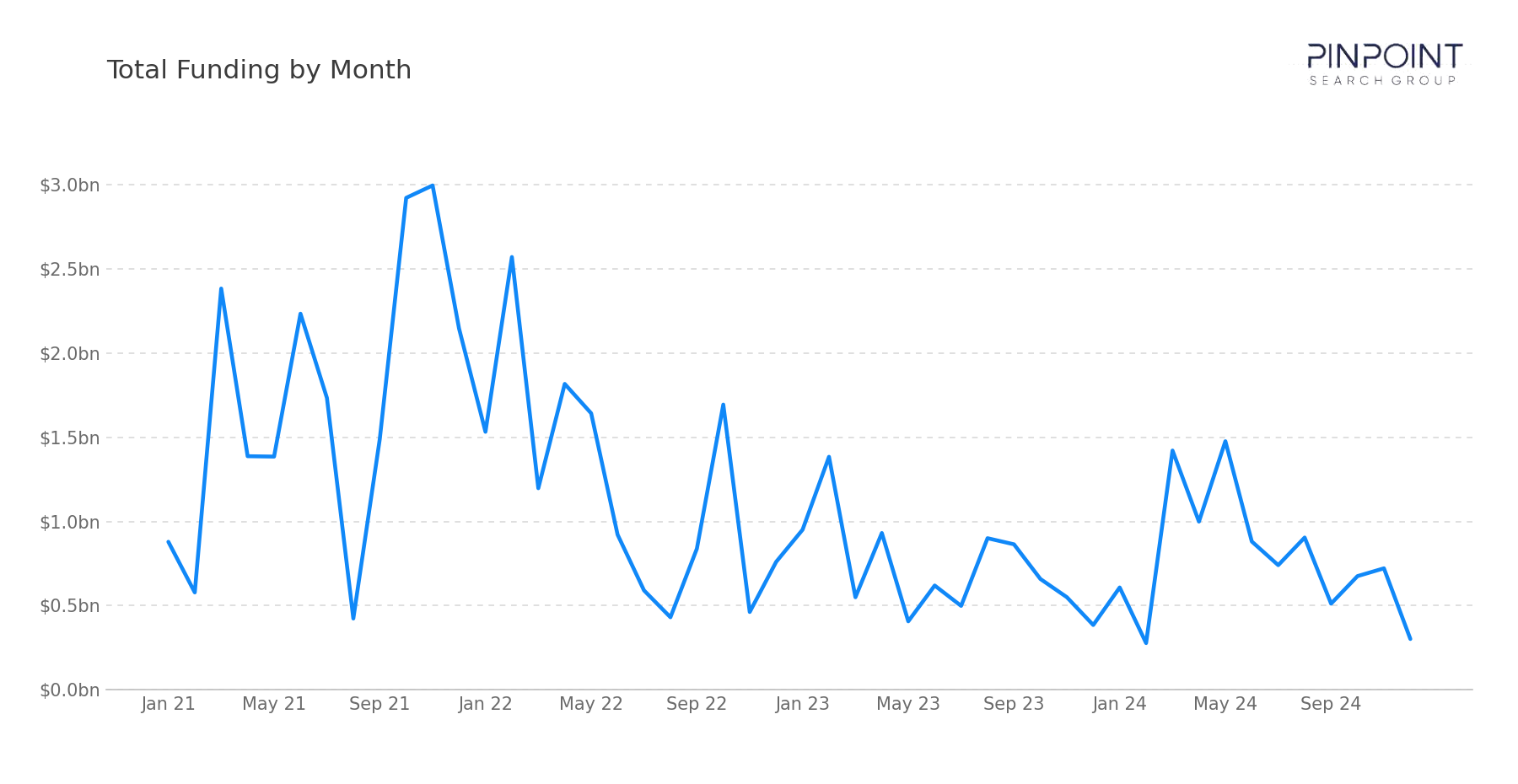

Funding recovered unevenly in 2024. The $9.52 billion was up 9% from 2023, but the gain came from a handful of large rounds rather than a broad reflation. Quarterly funding peaked at $3.36 billion in Q2 and settled to $1.7 billion by Q4.

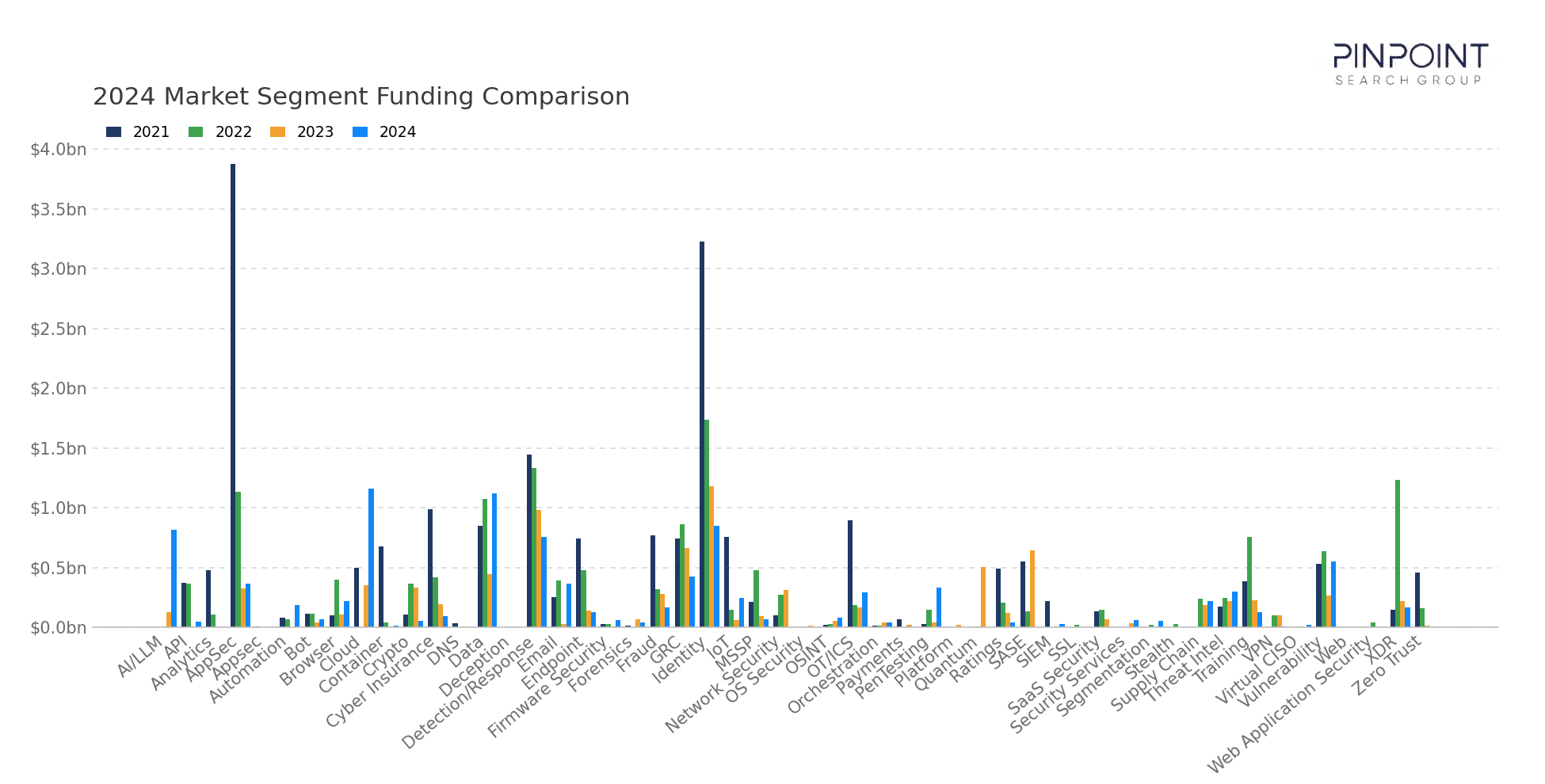

Capital concentrated in cloud, data, and the emerging AI-security category:

- Cloud security drew the largest round — Wiz's $1 billion Series E, the year's biggest by a wide margin, with Kiteworks' $456 million growth round (data) behind it.

- AI security emerged as its own category — Cyera raised twice ($300 million growth and $300 million Series D), classified under AI/LLM, as the security implications of AI moved into focus.

- Data security stayed well-funded — $1.12 billion across 38 rounds.

- Late-stage names returned — Abnormal Security ($250 million), Axonius ($200 million), Armis ($200 million), and Island ($175 million) reflected renewed conviction in established platforms.

The recovery was real but narrow — fewer, larger, more selective rounds, with the early-stage base steady at 59% of volume. 2024 read as the start of a disciplined reflation.

Market & Macro Signals

Four dynamics shaped 2024 — and for the first time, AI security carried genuine macro weight.

The acquirer base broadened. The year's M&A spanned PE take-privates (Darktrace), PE platform roll-ups (AuditBoard), a deepening non-cyber strategic (Mastercard/Recorded Future), and pure-cyber strategics (CyberArk/Venafi) — no single buyer type dominated.

AI security became investable. Cyera's two $300 million rounds and a wider wave of AI-security startups marked the point where the category drew dedicated late-stage capital, as enterprises grasped the security implications of AI adoption.

Late-stage conviction returned selectively. Wiz's $1 billion round and other nine-figure deals showed capital willing to back scale again — but only in a few names.

Consolidation spread across cohorts. Darktrace, AuditBoard, Recorded Future, Venafi, and SecureWorks all changed hands, extending consolidation well beyond the identity focus of 2022.

M&A Activity & Strategic Moves

Disclosed M&A reached $17.21 billion across 22 priced transactions (of 75 total). The defining feature was breadth of buyer type rather than a single dominant cohort. The largest deal was Thoma Bravo's $5.3 billion take-private of Darktrace.

The priced deals partition across cohorts:

- PE take-privates and platform roll-ups led. Darktrace to Thoma Bravo ($5.3 billion) and AuditBoard to Hg ($3 billion) put PE-aligned buyers — roughly $8.3 billion combined — at the top of the dollar table.

- A non-cyber strategic deepened its position. Mastercard's $2.65 billion acquisition of Recorded Future extended the payments network further into threat intelligence, building on its earlier identity and fraud acquisitions.

- Pure-cyber strategics consolidated capability. CyberArk/Venafi ($1.54 billion, machine identity) and Sophos/SecureWorks ($859 million, XDR) folded adjacent capability into existing platforms.

- The mix was unusually balanced. PE-aligned dollars, a non-cyber strategic, and pure-cyber strategics together made for the most diversified acquirer mix of the period.

The 2024 reframe is the breadth of the acquirer base. Where 2022 was PE-led identity consolidation and 2023 was one giant strategic deal, 2024's consolidation came from several directions at once — a sign of how many types of buyer now treat cybersecurity as core.

The public markets also reopened: Rubrik's April IPO was the first cyber-vendor listing the workbook tracked since the 2021 wave, ending a multi-year drought in new cybersecurity offerings.

Looking Ahead

2024 closed with funding in a disciplined recovery and consolidation broadening across buyer types.

Three themes carry into 2025:

- Whether the late-stage recovery accelerates — 2024's gains came from few rounds; a broader reflation would change the picture.

- Whether AI security sustains its momentum — the category drew real, dedicated capital in 2024 for the first time.

- Whether the broadened acquirer base persists — PE, non-cyber strategics, and pure-cyber buyers all stayed active through the year.

2024 was the year the recovery began and the acquirer base widened. Into 2025, expect continued selectivity in funding, growing weight on AI security, and consolidation from an unusually broad set of buyers.

The full 2024 dataset — every named company, round, investor, segment, and acquisition — is in the data feed. Get the full 2024 dataset →

Methodology

Every transaction in this report was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available. Figures are workbook-derived and reflect ongoing corrections, so they may differ slightly from the originally published 2024 report.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.