2025 Cyber Security Vendor Funding Report

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

2025 Cyber Security Vendor Transaction Highlights

Get the full 2025 dataset — every named company, round, investor, segment, and acquisition.

Crunching the Numbers

- The $13.97B raised in FY 2025 represents a 47% increase in funding raised compared to 2024 ($9.52B).

- Funding volume increased by 28% with 393 funding rounds tracked in FY 2025 compared to 307 in 2024.

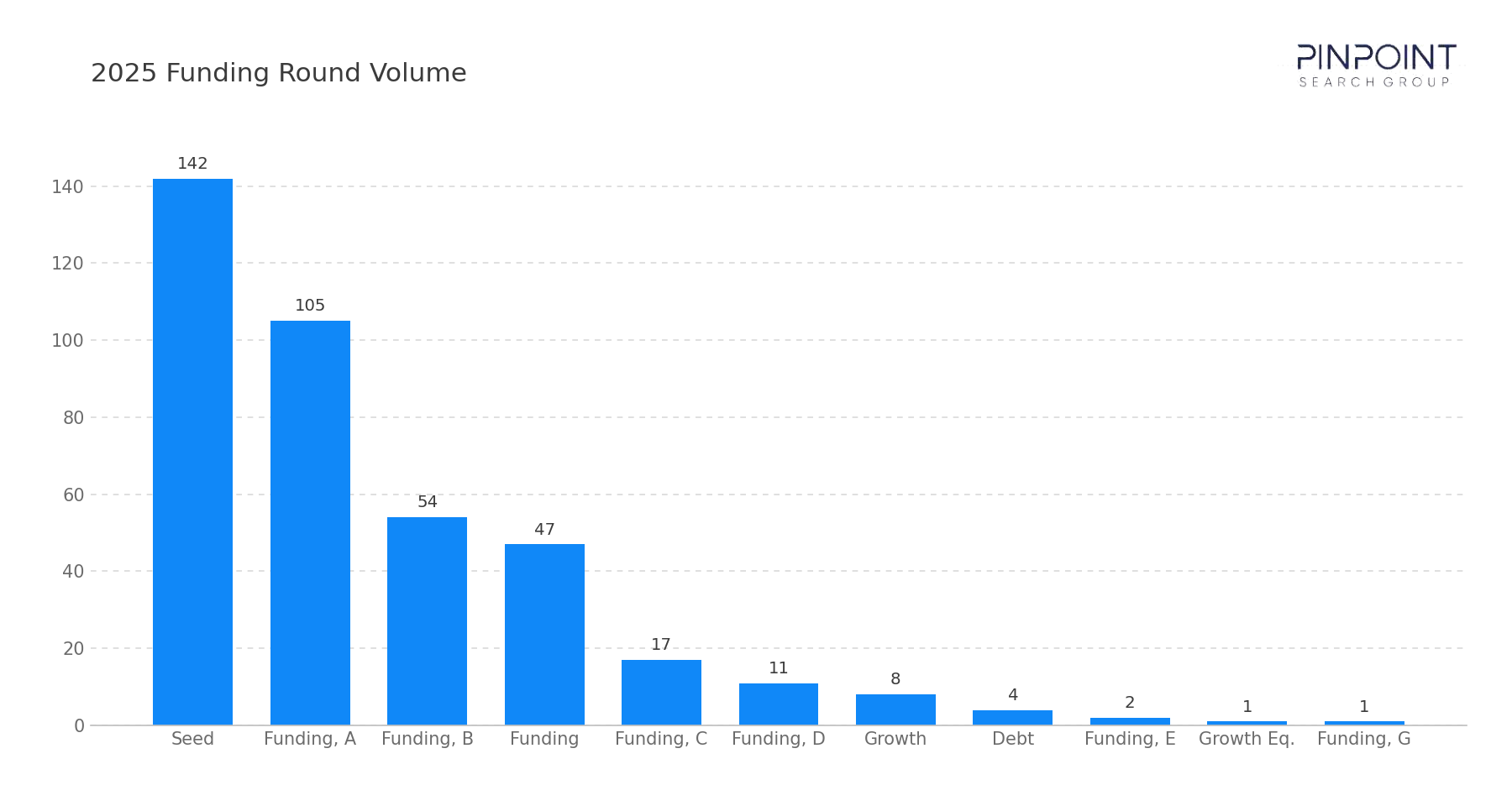

- Early-stage funding (Seed, Series A) represented 63% of total funding volume.

- 30 funding rounds above $100M accounted for 49% of all capital raised while representing just 8% of funding volume.

Join our mailing list to receive quarterly report analysis

Highlights and Analysis

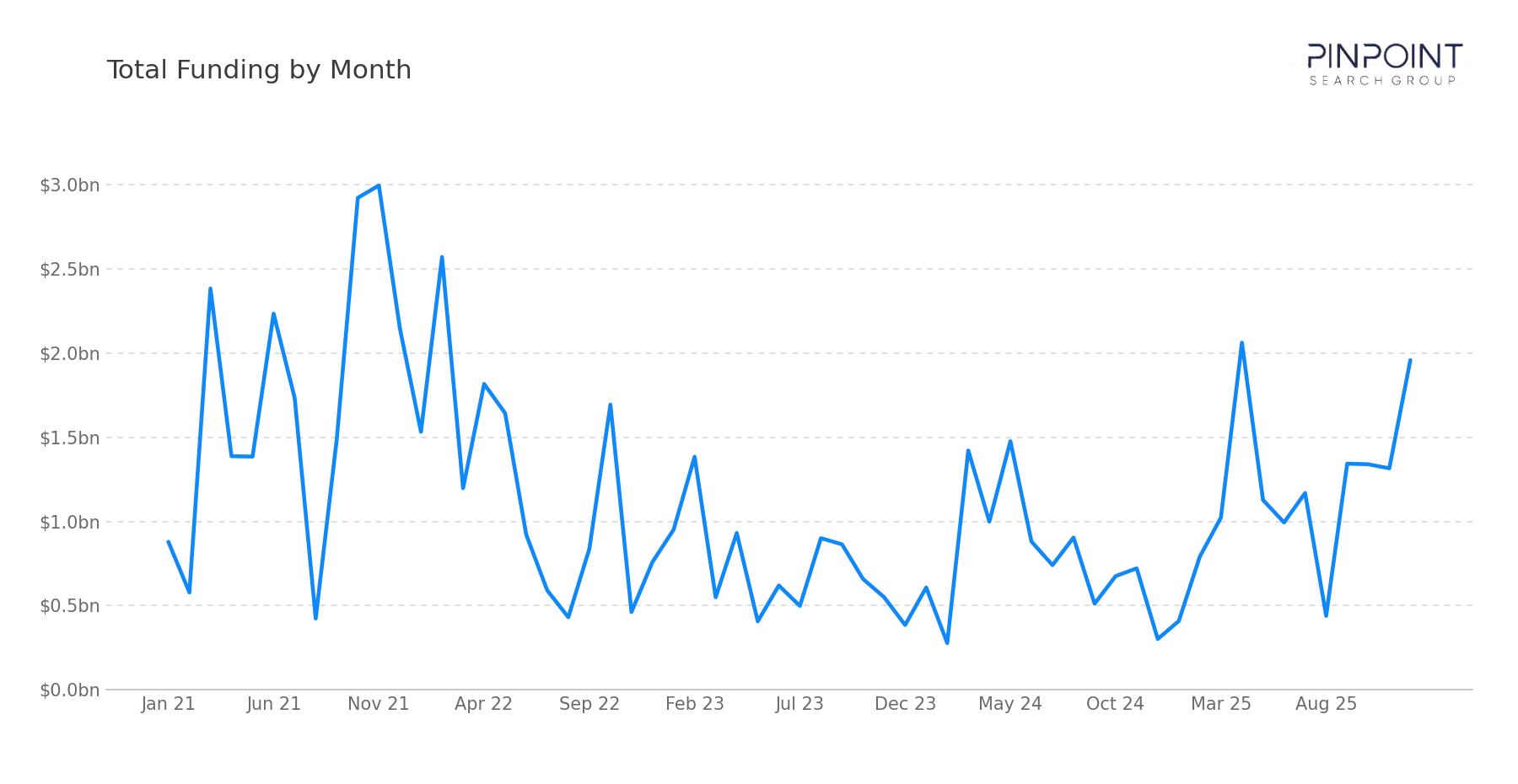

In 2025 our team tracked $13.97 billion in disclosed cybersecurity vendor funding across 393 rounds — a 47% increase over 2024 and the strongest funding year since the 2021 peak. The recovery that began to stabilize in 2024 accelerated in 2025, but the capital did not return indiscriminately. It returned with selectivity: more dollars, concentrated into fewer companies, paired with a higher bar for the businesses that received it.

The shape of the year is the story. Early-stage activity (Seed and Series A) accounted for 63% of all funding rounds, sustaining the broad formation of new companies that has defined the workbook since its first year. At the same time, 30 rounds of $100 million or more absorbed 49% of every dollar raised while representing just 8% of funding volume — the return of large, conviction-led late-stage rounds after two cautious years. Robust early-stage formation and concentrated late-stage capital coexisted in the same year. That combination reads as disciplined rather than defensive.

M&A told a parallel story. Strategic buyers concentrated on platform expansion, capability adjacency, and consolidation — most visibly in identity, AI-driven detection, and data security. The year's anchor transaction, Google's $32 billion acquisition of Wiz, was the largest cyber acquisition the workbook has tracked, surpassing the prior high (Cisco/Splunk, $28 billion in 2023). Around it, a steady run of mid-cap deals reinforced the same logic: acquirers were buying coherence, not just coverage.

Funding Overview

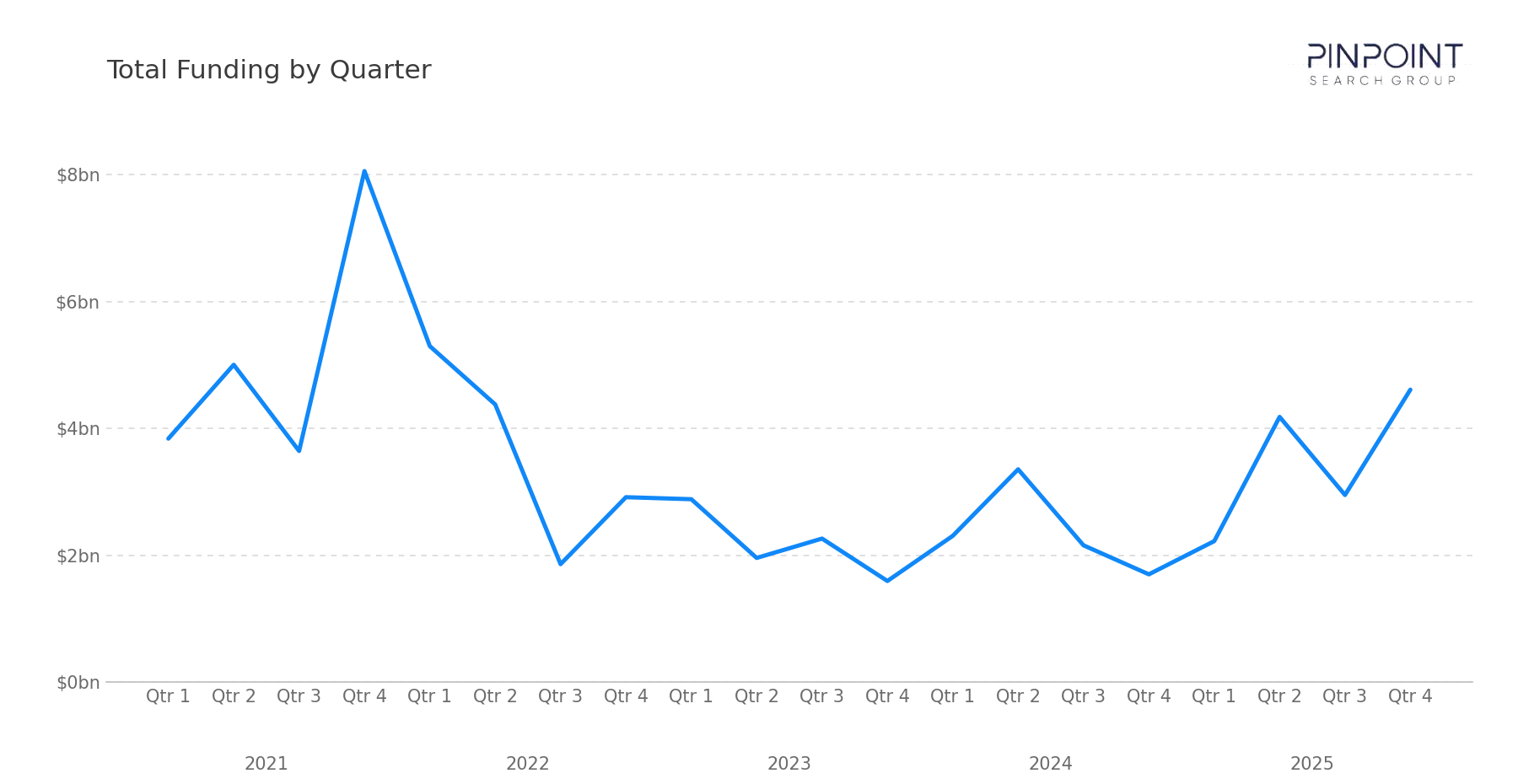

The 2025 funding total underscores how different this recovery looks from the last expansion. Capital flowed, but it flowed unevenly and intentionally. Funding built through the year, from $2.22 billion in Q1 to $4.61 billion in Q4, with the back half of the year carrying the heavier late-stage rounds.

Early-stage companies continued to represent a substantial share of overall activity. Seed and Series A together made up 63% of rounds, and the volume of new-company formation held up even as total dollars concentrated higher in the stack. Where capital found scale, it did so in a small number of large rounds clustered in the categories buyers were also consolidating:

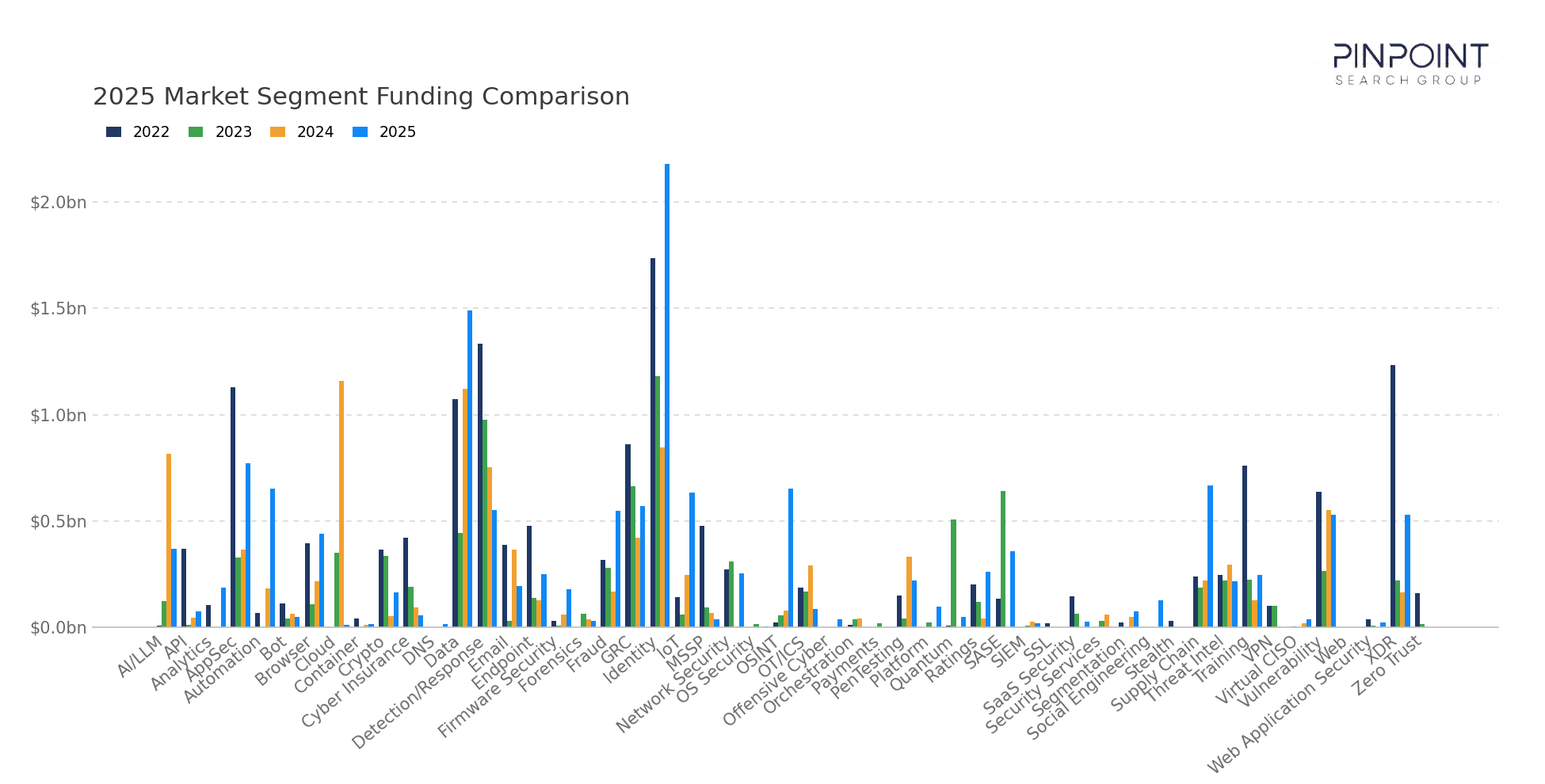

- Identity led the year on disclosed funding — $2.18 billion across 42 rounds, anchored by Saviynt's $700 million Series B, ID.me's $340 million round, and Persona's $200 million Series D. Identity was both the most-funded category and the most-acquired.

- Data security drew the second-largest pool — $1.49 billion across 33 rounds, with Cyera raising twice in the same year ($500 million and $400 million) as cloud data security pulled repeat conviction from investors.

- Late-stage platform rounds concentrated capital — ReliaQuest's $500 million growth round (XDR), Cato Networks' $359 million (SASE), and Chainguard's two rounds totaling $636 million (supply chain) show capital backing companies already at scale.

- Early-stage volume stayed broad — 142 Seed and 105 Series A rounds spread across more than 40 segments, the wide base of formation that the concentrated late-stage rounds sit on top of.

Founders raising in 2025 faced a more demanding bar — clearer articulation of the problem, credible go-to-market, and relevance to a consolidating ecosystem. The coexistence of broad early-stage formation and concentrated late-stage investment is what defines the current market. It is disciplined, not defensive.

Market & Macro Signals

Several macro trends help explain where capital flowed in 2025, and why.

AI adoption is outpacing governance and identity controls. As enterprises deployed AI faster through 2025, the gap between adoption and the governance, identity, and control frameworks meant to contain it widened. Capital responded: GRC and AI-governance positioning recurred across the funding base, and buyers paid up for AI-security capability (Palo Alto Networks/Protect AI at $700 million, CrowdStrike/Pangea at $260 million, F5/CalypsoAI at $180 million).

Identity remained the control plane for modern risk. Cloud complexity, AI access, and third-party connectivity kept identity as the primary point of enforcement. It led the year in both funding ($2.18 billion) and acquisitions, the clearest signal that the market treats identity as the layer where security decisions are enforced.

Fraud, OT/ICS, and critical infrastructure stayed in focus. Industrialized digital fraud and rising scrutiny of operational technology drew continued investment and M&A — Mitsubishi Electric's $1 billion acquisition of Nozomi Networks and Armis's $120 million purchase of OTORIO both pointed capital at the OT/ICS layer.

Budgets are rising, but concentration is increasing. Enterprise security spend kept growing while consolidating into fewer vendors and larger contracts. The funding data mirrored it: 30 rounds absorbed nearly half of all capital. Platforms able to deliver measurable outcomes drew disproportionate investment.

M&A Activity & Strategic Moves

M&A in 2025 reflected the same forces shaping funding. We tracked 71 acquisitions, 26 with disclosed values totaling $55.35 billion. Strategic buyers focused on platform expansion, capability adjacency, and consolidation — concentrated in identity, AI-driven detection, and data security. The year's defining transaction was Google's $32 billion acquisition of Wiz, the largest cyber acquisition the workbook has tracked.

Beyond the Wiz deal, the disclosed transactions clustered around a familiar set of buyers and themes:

- Platform players widened beyond pure cyber. ServiceNow made two cyber acquisitions in the same year — Armis at $7.78 billion (IoT/OT) and Veza at $1 billion (identity) — extending a non-cyber platform vendor materially into the security stack.

- Data security consolidated. Palo Alto Networks/Chronosphere ($3.33 billion), Veeam/Securiti ($1.73 billion), and SentinelOne/Observo AI ($225 million) concentrated capital into the data layer that also led funding.

- Identity was bought as often as it was funded. ServiceNow/Veza ($1 billion), CyberArk/Zilla Security ($165 million), and Okta/Axiom ($100 million) reinforced identity as the year's most-contested category.

- AI-security capability commanded a premium. Palo Alto Networks/Protect AI ($700 million), CrowdStrike/Pangea ($260 million), and F5/CalypsoAI ($180 million) show acquirers paying to fold AI-security into existing platforms rather than build it.

The throughline is consolidation toward coherence. Acquirers were not buying coverage for its own sake; they were assembling control coverage, visibility, and time-to-value into platforms enterprise buyers could standardize on. M&A increasingly functioned as an enabling layer inside broader security architectures rather than as a set of standalone product additions.

Two vendors also exited to the public markets in 2025 — SailPoint in February and Netskope in August — the first paired listings the workbook has tracked since the 2021 wave, after Rubrik reopened the cyber IPO window in 2024.

Looking Ahead

2025 was the strongest post-2022 funding year. The volume is there, but it is increasingly directed.

Three areas are positioned to draw capital and buyer attention into 2026:

- Early-stage vendors with credible teams and fast iteration — the broad Seed/Series A base remains the formation layer, and the bar for breaking out of it is rising.

- Growth-stage platforms that offer post-consolidation control coverage — the late-stage rounds that concentrated capital in 2025 favored companies already operating at platform scale.

- AI-native startups where automation delivers measurable buyer value — the premium acquirers paid for AI-security capability in 2025 signals where strategic demand is heading.

As the market moves into 2026, we expect continued selectivity, increased diligence on go-to-market, and tighter alignment between budget allocation and board-level priorities. Capital is available, but it is moving differently — concentrated, conviction-led, and pointed at the categories where consolidation is already underway.

The full 2025 dataset — every named company, round, investor, segment, and acquisition — is in the data feed. Get the full 2025 dataset →

Methodology

Every transaction in this report was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available. Figures are workbook-derived and reflect ongoing corrections, so they may differ slightly from the originally published 2025 report.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.