January 2024 Cyber Funding & M&A Brief

Published by Pinpoint Search Group — the cybersecurity executive search firm that tracks every disclosed vendor funding round and acquisition in the sector.

At a glance

Get the full January 2024 dataset — every named company, round, investor, and segment.

What January told us

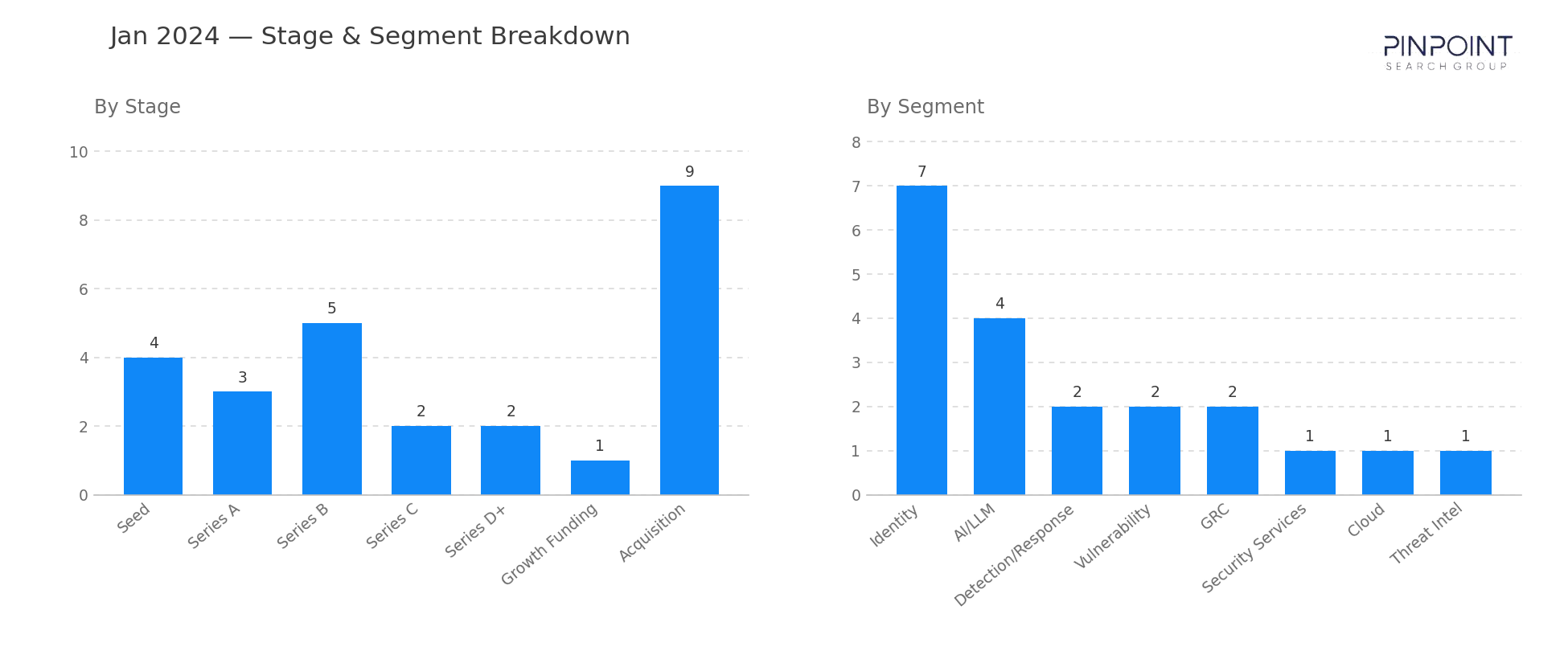

January 2024 opened the year with 26 transactions and $608M in disclosed funding capital — a measured restart after a flat second half of 2023. Identity led the segment mix with 7 of the month's transactions, and the funding stack skewed late-stage: Silverfort's $116M Series D and Aqua Security's $60M Series D arrived alongside ExtraHop's $100M growth round, signaling that capital was still flowing to platform vendors with established enterprise traction even when earlier-stage activity stayed muted.

M&A was busy but mostly quiet on price. Nine acquisitions cleared in January and only one — SentinelOne's $100M deal for PingSafe — came with a disclosed value. The undisclosed seven include Dynatrace acquiring Runecast, Mimecast picking up Elevate Security, SonicWall acquiring Banyan Security, and Delinea taking Authomize. The throughline is platform consolidation: every named acquirer here was folding a point capability into a broader product line rather than entering a new category outright.

Inside Identity, the named rounds skewed toward non-human and workload identity (Oasis Security's $35M Series A, Silverfort's broader machine-identity expansion at Series D, Aqua's container-runtime identity controls). The pattern is consistent with the broader trend visible across late 2023: as workforces stabilized, capital migrated to the parts of identity that are still growing — service accounts, agents, and the workloads themselves.

Stage and segment breakdown

| Stage | Count |

|---|---|

| Seed | 4 |

| Series A | 3 |

| Series B | 5 |

| Series C | 2 |

| Series D+ | 2 |

| Growth Funding | 1 |

| Acquisition | 9 |

| Top segments | Transactions |

|---|---|

| Identity | 7 |

| AI/LLM | 4 |

| Detection/Response | 2 |

| Vulnerability | 2 |

| GRC | 2 |

| Security Services | 1 |

Two deals worth your attention

Silverfort — $116M Series D in Identity. Silverfort's unified identity protection platform extends MFA and conditional access to legacy systems and service accounts that other identity vendors can't reach. The Series D was the single largest funding event of January and continued an unbroken arc — $30M Series B in 2020, $65M Series C in 2022, $116M Series D in 2024 — across one of the longest-running identity stories in the workbook.

SentinelOne's $100M acquisition of PingSafe. SentinelOne folds PingSafe's cloud-native application protection platform into its broader endpoint and cloud security stack. PingSafe had only raised a $3.3M Seed in mid-2023, making this a fast Seed-to-strategic exit at a roughly 30x markup — early evidence that 2024's M&A market was willing to pay for cloud-security capability even before companies hit Series A.

Companies we've covered before

Aqua Security first appeared in May 2020 with a $30M Series D in the then-named Container segment, returning in March 2021 with a $135M extension at the same stage. The January 2024 $60M Series D refresh keeps Aqua in the workbook as one of only a handful of vendors with three+ disclosed rounds at the D-stage line — and a marker for how the Container segment language quietly rolled into Cloud over the same period.

PingSafe first appeared in July 2023 with a $3.3M Seed in Detection/Response. Six months later, the company exits to SentinelOne for $100M — one of the shorter Seed-to-acquisition arcs we've tracked, and a useful early-2024 data point for how cloud-security capability is being priced inside strategic windows.

The other 24 transactions are in the data feed — including the 9 acquisitions whose values never hit the press. Get January's details and more →

Methodology

Every transaction in this brief was sourced from a primary public report and dedupe-checked against the master Pinpoint funding workbook, which now contains ~2,600 transactions back to May 2020. Funding totals reflect disclosed capital only; acquisition values are included where publicly available.

Each deal is classified against Pinpoint's normalized cybersecurity segment taxonomy — read directly off what the company says they protect and mapped to one of the canonical segments. The taxonomy has been maintained continuously since 2020 and currently covers roughly 55 segments. Identity, Data, Detection / Response, and Threat Intel have been tracked from the first month of the series; AppSec and GRC entered the following month; emergent categories (AI/LLM, Supply Chain, Quantum, Browser) are added when they first appear in vendor positioning. That normalization layer is what makes multi-year, cross-segment comparisons possible against an otherwise inconsistent vocabulary in the broader market.

About Pinpoint Search Group

Cybersecurity innovators work with Pinpoint Search Group to identify, attract, and land professionals that enable maturation, scale, and successful outcomes. As start-ups continue raising millions in funding and established vendors make acquisitions to round out their offerings, Pinpoint Search Group is keeping track.

Get the underlying data

The narrative above is the free version. The paid Pinpoint Cyber Funding Data feed gives you every named transaction, every disclosed investor, every segment classification — exportable, filterable, and updated as the deals close.